Most contractors meet performance bonds when a public owner or prime contractor makes them a condition of award. You can build for years without one, then a city bid or Fortune 500 client requires a bond and the game changes overnight. You are now dealing with a surety underwriter who cares about your track record, your financials, and, yes, your credit score. Understanding how these pieces fit together saves time, unlocks bigger projects, and prevents awkward surprises right before bid day.

What a Performance Bond Actually Is

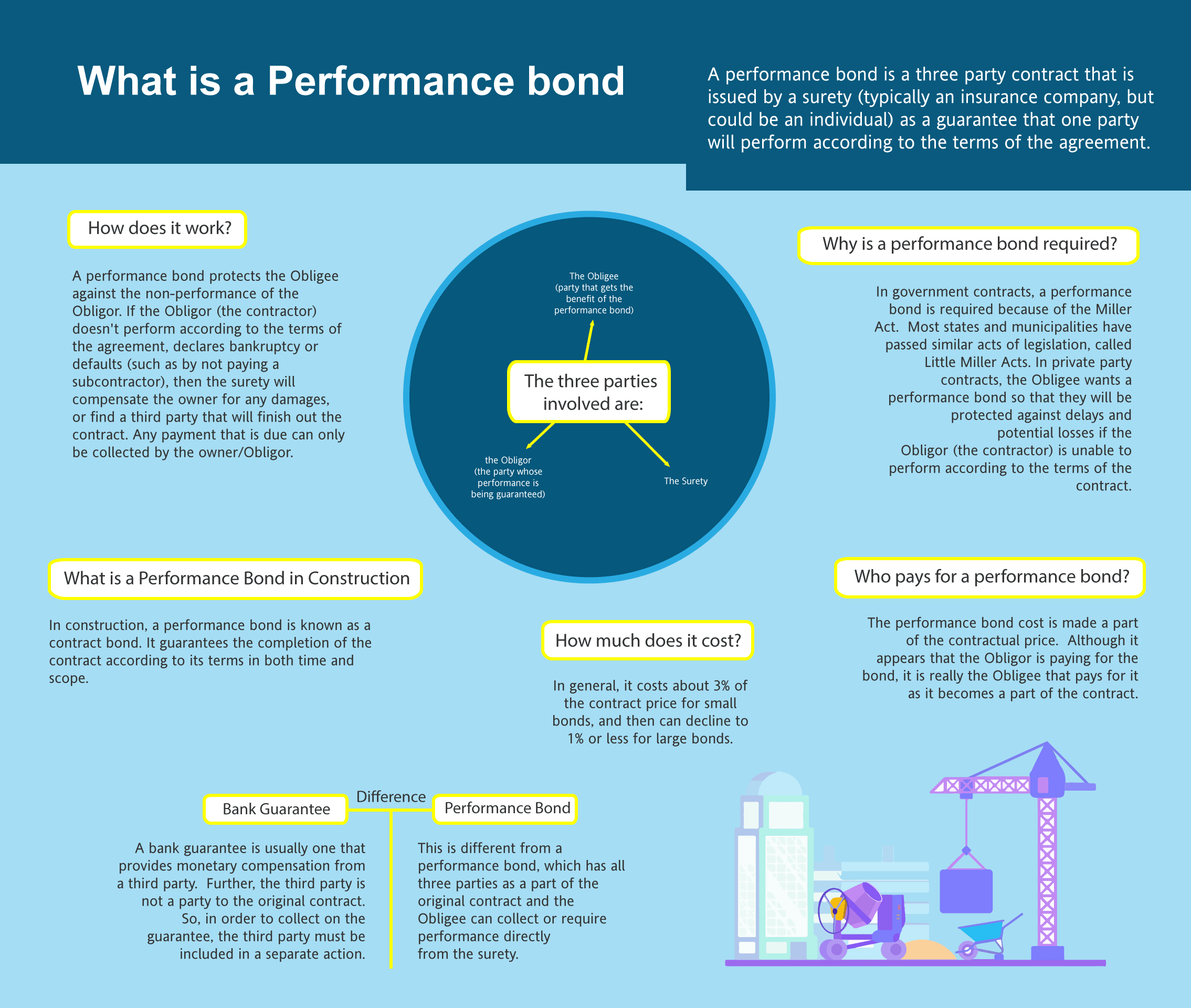

A performance bond is a three-party agreement used mainly in construction and other contract work. The surety company guarantees to the project owner that the contractor will complete the job according to the contract. If the contractor fails to perform, the owner can make a claim on the bond. The surety then steps in, investigates, and, if the claim is valid, finances completion, hires a replacement contractor, or compensates the owner up to the bond’s penal sum.

The language matters. Unlike insurance that expects losses and prices accordingly, surety is underwritten on the assumption of no loss. The surety evaluates whether you can and will fulfill your contract. If they pay a claim, they expect to be repaid by the contractor through an indemnity agreement, typically a general agreement of indemnity signed by the contractor and often its owners.

In practice, performance bonds usually pair with payment bonds, especially on public work. The payment bond guarantees that subs and suppliers will be paid, which keeps liens off the project. Many owners require a performance and payment bond equal to 100 percent of the contract amount.

Why Owners Require Them

Owners use performance bonds to transfer risk. They want assurance that a low bid will not turn into a half-built structure and a legal mess. Public owners are often required by statute to obtain bonds on large jobs, a legacy of the Miller Act at the federal level and “Little Miller Acts” in the states. Private owners and general contractors use bonds to protect schedules, lenders, and reputations.

From the owner’s view, the bond functions as an emergency plan. If a contractor walks off, goes insolvent, or falls hopelessly behind, the surety has both the resources and the duty to resolve the problem. Even when a claim never occurs, the underwriting process screens out unqualified bidders and imposes discipline on project selection and financial management.

How the Surety Relationship Works

When you apply for a bond, you start a relationship with a surety underwriter. If you are new to bonding, this feels a lot like a bank loan process with added emphasis on construction acumen. You submit financial statements, contract history, work-in-progress schedules, bank references, and resumes of key people. For larger programs, sureties ask for CPA-reviewed or audited financials and sometimes a lines-of-credit letter from your bank.

The surety looks at the “three Cs” of underwriting: character, capacity, and capital. Character covers your reputation, claims history, and whether you keep your word. Capacity means you have the people, equipment, and systems to execute the work you are taking on. Capital, the big one for many, measures financial strength, cash flow, and working capital to absorb delays, retainage, and change orders.

Unlike a one-off loan, a bonding program operates as a line of credit measured in aggregate and single-job limits. An underwriter might start you at, for example, $750,000 single and $1.5 million aggregate, then grow that line as you build a track record.

Premiums, Rates, and What You Actually Pay

Performance bond premiums typically land between 0.5 percent and 3 percent of the contract amount, with the biggest factor being the contractor’s risk profile and the job’s size and type. Larger contracts benefit from stepped rates that reduce the marginal rate on dollars above a certain threshold. Premiums are paid up front or per project, not monthly like insurance.

If you hear a flat rate quoted over the phone without questions, be careful. Real pricing depends on underwriter judgment and the documentation you provide. Highly qualified contractors with strong financials may see rates under 1 percent for standard work. Startups with thin capital might pay closer to 3 percent, sometimes on a collateralized basis.

Claims and What Really Happens When a Job Goes Sideways

Owners do not get to collect on a bond just because they are frustrated. A valid default requires specific contract failures and usually formal notice requirements. The surety investigates both sides, assesses cure options, and chooses among several responses: finance the original contractor to finish, bring in a completion contractor, or pay the owner for the documented excess completion cost up to the bond limit.

Every claim, even if resolved without payment, leaves a footprint. It will be discussed in future underwriting. Underwriters watch not only the cause of the problem but how the contractor communicated and cooperated. If the surety pays, they will seek reimbursement from the contractor under the indemnity. That is often a multi-year workout if the loss is large.

Where Credit Score Fits Into Underwriting

The phrase what is a performance bond tends to draw people into mechanics and statutory rules. Credit score seems like a minor detail until you apply and discover it sets the tone for your file. For small and mid-size contractors, personal credit of the owners is one of the fastest predictors of how the business treats obligations and handles pressure. Underwriters do not rely on credit score alone, but it influences how much documentation is required, whether collateral is requested, and the limits offered.

For bonds up to roughly $500,000 to $1 million, many sureties use streamlined programs. A strong personal credit score can unlock quick approvals with limited paperwork. On the other hand, weak credit often bumps you into a full-file underwriting lane that asks for CPA statements, tax returns, and more detail. Above $1 million, everyone is in full-file territory regardless of credit, but credit quality still shades decisions.

From experience, here is a fair translation of typical credit tiers into underwriting posture. Exact cutoffs vary by surety, region, and time.

- 750 and up: green light for most standard program starts, limited documentation on smaller jobs, competitive rates 700 to 749: acceptable with standard documentation, good chance at clean approvals and step-ups in limits as performance builds 650 to 699: doable, but the underwriter will look harder at financial statements and banking; expect conservative single and aggregate limits at first 600 to 649: possible with compensating strengths like strong working capital, collateral, or a co-indemnitor; higher rates common Below 600: difficult for performance bonds beyond very small jobs; collateral, funds control, or a specialty market might be required

Credit score is a proxy, not destiny. Underwriters look for patterns. A single late payment from five years ago will not carry the same weight as ongoing collections activity. Tax liens raise more alarm than a disputed cell phone bill. Bankruptcies, especially recent ones, are a major hurdle but not a permanent bar if the business has reestablished solid financial footing.

What Underwriters Actually Read in a Credit Report

Underwriters review credit reports differently than consumer lenders. They look for context. A medical collection may be noted then discounted if the rest of the file is clean. A pattern of high utilization on personal credit cards used to float business expenses, though common, signals thin capital and cash management stress. A judgment or tax lien forces the question of unbonded liabilities that could prime project cash.

The report also shows stability markers. Length of credit history, the presence of installment loans paid as agreed, and a low ratio of revolving balances to limits all build confidence. They align with the idea of character in the three Cs, the habit of meeting obligations even in slow months.

How Credit Interacts With the Other Two Cs

Capacity and capital can compensate for mediocre credit, to a point. A contractor with average credit could still receive approval for a $2 million bond if the company holds $800,000 of working capital, owns its equipment free and clear, and has a track record of profitable, similar-size jobs with on-time completion. Conversely, stellar credit will not carry a contractor with weak financials into oversized work. Think of credit as the front door. Strong credit opens it easily. Weak credit means you need more proof in hand when you knock.

Managing Around Credit Weakness

If your credit score is not where you want it, you still have paths. Surety is relational. Underwriters remember contractors who clean up issues and follow through on plans.

- Provide context early. A brief, honest letter that explains a dip in credit following a health event or divorce helps frame the report. Strengthen your financial presentation. CPA-reviewed statements, a clean WIP schedule, and a bank line of credit with a letter of support calm nerves. Offer incremental growth. Start with smaller bonded jobs, close them profitably, and ask for raises in your single and aggregate limits. Consider funds control. Agreeing to third-party funds disbursement protects subs and materials payments, which can allow approvals even when credit is soft. Use collateral strategically. Pledging a CD or cash margin is not anybody’s first choice, but it can bridge to approvals for time-sensitive projects while you continue improving fundamentals.

These are not magic tricks. They trade convenience and sometimes cost for the ability to secure performance bonds while you rebuild your credit standing.

Practical Example From the Field

A midsize site contractor I worked with, call them Riverbend, had grown nicely on private work without bonds. A county RFQ for a $3.2 million road project required performance and payment bonds. The owners’ personal credit scores sat around 645, pulled down by several late payments during a drought year when they used personal cards to cover payroll.

Their CPA-prepared statements showed $1.1 million in equity, but only $420,000 in working capital after retainage and underbillings. The surety hesitated on the size given their bonding history and the credit signals, even though their past performance was strong.

We built a package that included a bank letter confirming a $750,000 working capital line, an agreement to enroll the project in funds control with joint checks to critical suppliers, and a collateral pledge of a $100,000 CD that More help would release at 50 percent completion. The surety approved the bond. Riverbend finished with a 6 percent gross margin, paid the line down, and asked for higher limits the next season. By then, the owners’ scores had climbed past 690, and the surety released the collateral requirement.

The point is not that everyone needs collateral. It is that credit nudged the underwriter to look for structure. With the right structure, you can move forward while improving your file.

How To Prepare Your Bond File So Credit Is Not the Only Story

Underwriters are efficiency-driven. If you make the decision easy with a coherent, complete package, credit becomes a single data point among many, rather than the headline.

Here is a concise preparation checklist that fits most first-time or growing programs.

- Latest CPA-prepared financial statements with notes, plus interim statements no older than 90 days A current work-in-progress schedule showing contract amounts, cost to date, billings, and estimated cost to complete Bank information: availability on lines, average collected balance, any covenants, and a reference contact Resumes of key personnel and a project list highlighting five similar jobs with size, scope, and outcome A brief narrative on controls: job costing process, change order management, subcontractor selection, and safety record

If credit is a concern, include a one-page explanation with dates, amounts, and resolution status, and attach proof of payment or settlement where applicable. This stops back-and-forth and shows ownership of the issue.

The Role of Working Capital and Net Worth

Two financial metrics carry a lot of weight: working capital and net worth. Working capital is current assets minus current liabilities. Sureties often use rules of thumb that translate working capital into single-project and aggregate capacity, subject to judgment. A comfortable starting point might look like single job limits at one to two times adjusted working capital and aggregate limits at about two to three times, though the mix of jobs and the accuracy of cost-to-complete figures can move those numbers.

Contractor net worth supports resilience. Equity that is not just goodwill, but cash, receivables that turn, and unencumbered equipment, gives underwriters confidence that you can weather change orders stuck in approval, retainage delays, and the occasional ugly surprise underground. When credit is borderline, stronger working capital and equity can lower perceived risk enough to win approval.

Why Some Contractors Get Approved Quickly

Speed comes from alignment. When an owner’s personal credit is north of 700, the CPA statements reconcile to tax returns, the WIP schedule ties to the ledger, and the bank letter confirms liquidity, underwriters move fast. They can see the full picture in one pass, price the risk, and focus on whether the project itself fits your experience.

Contrast that with a file that has missing pages, stale financials, unexplained draws, and a credit report dotted with recent lates. The underwriter cannot price that without multiple follow-ups. Time kills deals, and time tends to accrue on weaker files precisely when deadlines are tightest.

What If Your Credit Is Good But You Still Get Pushback?

Healthy credit does not override project-specific concerns. Sureties recoil at thin margins on risky scopes, unfamiliar geographies, stacked schedules with too many concurrent starts, or owners with payment reputations that worry them. A perfect 800 credit score will not erase a 3 percent gross margin on a winter bridge deck with a compressed timeline.

If you face pushback despite good credit, rework the plan. Bring in a specialty sub for the riskiest scope. Improve cash flow by negotiating better progress payment terms or front-loading mobilization. Add a superintendent with deep experience in that type of work. Or pass on the job and wait for a cleaner fit that grows your program without gambling your relationship.

The Cost of Ignoring Credit Until Bid Day

I have seen more than one contractor assemble a winning estimate, submit the bid, then discover that the bond line is too small or the surety will not approve the job as structured. Missing a deadline for the bond or trying to swap in a different surety at the eleventh hour rarely ends well. The owner loses confidence, your subs get jittery, and you may forfeit a bid bond if you cannot execute the contract.

Make prequalification part of your annual planning. Meet with your surety agent, review your backlog and pipeline, and discuss target sizes for the next season. If credit work is needed, start months ahead. Removing a single 90-day-old collection from your report or paying down revolving utilization at statement cut dates can shift your score by 20 to 40 points, which can change the underwriter’s posture.

How Credit Scores Move and What Changes Fast

Credit scores react to both errors and habits. Disputing a misreported late payment can yield a quick lift once the bureau updates it. Paying down card balances below 30 percent of limits, especially before the statement date so the reported balance is lower, can move the needle within a cycle or two. Setting up auto-pay for minimums will prevent future accidental lates, which underwriters interpret as sloppiness more than malice.

The slow fixes are bankruptcies, tax liens, and major charge-offs. Those require documented settlements and time. A surety may proceed with protections like funds control while those age off, but count on conservative terms until the paper trail shows closure.

Specialty Markets and When To Consider Them

There are sureties that focus on nonstandard credit or early-stage contractors. They price for the added risk and often require more structure, but they are legitimate avenues when mainstream markets decline. A common path is to use a specialty surety for a season or two while you clean up credit and grow working capital, then move into a standard market to reduce rates and loosen controls.

Your agent’s relationships matter here. A broker who knows which underwriters will read past a 620 score if everything else is solid can save weeks. Conversely, spraying applications indiscriminately creates duplicate inquiries and the appearance of a shop-around problem that underwriters dislike.

Common Misconceptions About Performance Bonds

One misconception is that the bond protects the contractor. It does not. It protects the owner. The surety’s duty runs to the obligee, and the indemnity runs to the surety. You benefit indirectly through eligibility to bid and the discipline of underwriting, but the bond is not your safety net.

Another misconception is that personal guarantees always disappear once you hit a certain size. In practice, most closely held contractors sign indemnity personally for their companies. Larger, institutionally backed contractors with audited financials and deep equity may negotiate limited indemnity or corporate-only indemnity, but that is the exception, not the rule.

A third misconception is that credit score does not matter if the company is strong. While business strength can outweigh mediocre credit, underwriters still read credit as a behavioral signal. Sloppy personal finance suggests potential sloppiness with change orders or payables, even if the corporate numbers look fine. It is a judgment factor, not a veto, but it shows up in files and in decisions.

Getting Strategic: Matching Projects to Your Bonding Profile

A smart approach is to build a ladder of projects that aligns with your current bonding capacity and credit posture. If you are just establishing a bond line and your credit sits in the mid-600s, target bonded jobs where you already have field expertise and supplier relationships, ideally in geographies where you know inspectors and permitting. Keep margins honest. A 7 to 10 percent gross margin on straightforward scopes beats a paper-thin number on a complex job that strains your credibility with the surety.

As your program and credit improve, push your single and aggregate limits with measured steps. Add complexity slowly, one new risk variable at a time. For example, take on a larger size while keeping the scope familiar, then later add a new scope but return to a mid-size job. Underwriters like patterns they can model. Show them you plan growth rather than chase it.

Final Takeaways for Contractors and Owners

If you came searching what is a performance bond, the core is simple: it is a guarantee that a contractor will finish the job as promised, backed by a surety that expects to be repaid if it has to step in. For contractors, the path to approval runs through the three Cs, with credit score acting as an early filter. Strong personal and business credit smooths the way. Weaker credit can be offset with substance, structure, and a transparent plan.

For owners and primes, knowing how sureties think helps you prequalify bidders realistically. Ask about their bonding program, current single and aggregate limits, and their relationship with their surety. A contractor who can explain their capacity, cash position, and past bonded performance in plain language likely has the controls to deliver for you.

The performance bond is not a bureaucratic hoop. It is a financial instrument that forces clarity. When you work with it instead of against it, projects get built, risks stay managed, and everyone sleeps better, including the underwriter reading your file.